Content

Europe’s Rare Earth dependence on China – Future Perspectives

The Future Now Show

Energy Innovation

Club of Amsterdam blog

News about the Future

Recommended Book: The Future of Continental Philosophy of Religion

The Asian Square Dance – 1st part

ISIS and Western intelligence role in the Middle East

Futurist Portrait: Geci Karuri-Sebina

Welcome to the ClubofAmsterdam Journal.

The first shows are online – with topics like climate change, food,social revolution, 3-D printing and medicine, marketing made meaningful, balanced communities and … The Future Now Show

Felix F Bopp, Founder & Chairman

Europe’s Rare Earth dependence on China – Future Perspectives

by Patrick Crehan

CEO and Founder, Crehan, Kusano & Associates

Director, Club of Amsterdam

Rare Earth Elements (REEs) form a group of 17 metals which play a very important role in modern industry, especially in the clean-tech and electronic sectors. Despite their name they are not really all that rare. However they are costly to extract, and sites from which their extraction makes commercial sense are relatively few and far between.

First discovered in Sweden in the late 1700s, they now play a very important role in modern industry as essential ingredients in:

- Energy Efficient Electrical Motors: A modern car can contain 60 electrical motors, doing all manner of things from adjusting the seats and the side-view mirrors to winding the windows up and down, controlling the air-conditioning and driving the windscreen wipers. REEs allow manufacturers to reduce their size and weight, while improving their energy efficiency. Modern electrical appliances for use at work or around the home try to be smaller and lighter cutting down on transport costs, while doing the same or better work using less energy.

- Wind Turbines and Hybrid Electric Cars: The generators of modern wind turbines contain many Tonnes of rare-earth metals. The turbine pictured below is produced by a Finnish company called Switch. Capable of generating 2.5MW, its permanent magnet is an alloy of neodymium and weighs 2000kg. About 30% of this by weight is REE.

- Speakers and Microphones: For example the small powerful energy efficient ones used in modern mobile phones.

- Other Uses: Disc drives, flat panel displays, the “phosphor” of traditional TVs and fluorescent light bulbs, new high efficiency light bulbs based on CFL and LED technologies, catalytic converters.

The picture below shows an example of a turbine for production of wind-energy. This particular model is produced by a Finish company called Switch. It has an output of up to 3.5MW and employs a permanent magnet containing 2,000 kg of REE alloy.

Modern mobile phones use small but essential quantities of REEs. Making the iPhone for example requires 9 different REEs in the screen and to polish the glass of the screen, in the microphone and vibration unit, as well as in its electronic circuitry. The following able was developed by CNET journalist Mark Hobbes.

It is easy to see why the demand for REES has developed very rapidly in the last few decades and is likely to continue to increase in future.

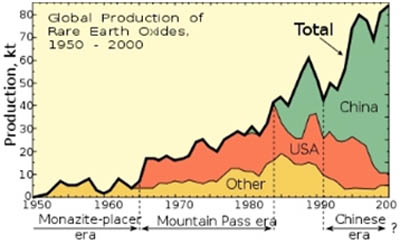

In 1990 China produced 27% of REEs and related minerals. By 2009, global production was of the order of 132,000 Tonnes of which China produced 129,000 Tonnes equal to almost 98% of global production. According to Wikipedia we are now in the “Chinese Era” of REE production.

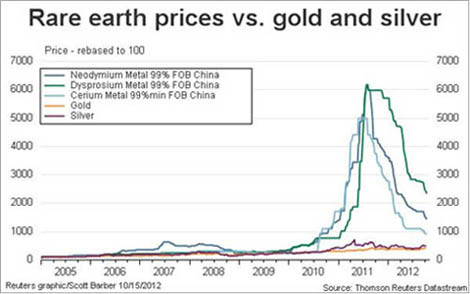

Things started to get tense however in about 2009 when China announced a plan to reduce exports of REES to 35,000 Tonnes per annum over the period 2010-2015, ostensibly to conserve scarce natural resources and protect the environment. This was followed up by a series of revisions of this policy, which in each case amounted to further limits on the export of REEs, including a total ban on exports to countries like Japan. The result was market chaos as prices rose out of control for a while and a number of REE consumers bought up reserves in a panic to ensure suppliers.

This began a period of trade tension between China and other countries including Japan, the US and Europe. Cases brought against China at the WTO, have ruled in favor of the plaintiffs and China is currently in the process of appealing the judgments.

In fairness, China is not only the biggest producers of REEs, it is also the biggest consumer. Demand for REEs has grown as fast in China as it has elsewhere. China also had very real concerns about the environmental damage and public health impact of illegal mining activities that had grown up in response to burgeoning domestic and international demand. According to a recent report published on the website of Rare Earth Investing News, 40% of magnetic REE mining supply in China is illegal. These activities are often mom-and-pop affairs described by one of the exports at the EIAS as an opportunistic situation where someone digs a whole in the ground, fills it full of sulphuric acid, waits a while, then scoops up a part of what is produced for further processing, before moving on to dig another hole without much care for the overall consequences on the environment, local water resources or the health of workers involved.

Other commentators such as The Economist have pointed out that export restrictions apply only to the raw materials and not to intermediate or finished goods. They observe that this is a very good strategy to help Chinese manufacturers move up the value chain, by “forcing” foreign manufacturers to outsource or relocate at least some of their manufacturing tasks to China. The case of General Motors moving its magnetic research facilities to China in 2006 has been put forward as evidence in support of this hypothesis.

The last word has not yet been printed on the WTO case against China. No doubt it will generate headlines in the months and years to come.

One of the main messages of the EIAS meeting was that the demand for REES has actually fallen since the crisis. One of the reasons put forward is that many who were in the market for REES are not permanently out because they have found other ways for doing what they did with REEs. Apparently this substitution effect has happened to some extent across all domains of application of REEs. It is possible also to imagine a natural fall-off in demand due to the global crisis that has reduced spending by individuals and by governments. Renewable energy policies for example should be seen as major drivers of demand for REEs based products. Another big driver should be overall global population growth. It seems that there is room to continue the conversation started at the EIAS and develop scenarios based on realistic assumptions about the impact of global growth, energy, environment and climate change policies on future demand for REEs.

Another major message coming out of the meeting seemed to be that nervousness concerning sources of REEs may be overblown. A representative of Molycorp, a major US producer of REEs based at Mountain Pass in California, pointed out that the Chinese share of production has fallen a long way from the highs of 2009 and 2010 and is now at about 82%, far from the 95% or 97% often quoted in the press. It seems many new sites are coming on line. Molycorp itself has made very important investments in its production facilities. To thoroughly re-invent and modernize its system of production based on in California it has had to obtain more than 500 permits. According to its representative, its new facilities are exemplars of industrial and environmental good practice, allowing it to produce at prices that are competitive with respect to China. Things look calm and stable for now and the pressure causes by Chinese limits on production and export is much lower for now. However the questions remain as to how long this might remain and what impact will growth and progressive policies in emerging economies have on demand and the adequacy of available supplies.

In the case of Japan, its reaction to the crisis of 2009-2011 includes initiatives to look into other sources of REEs, for example on the sea-bed. Already interesting prospects for commercially viable under sea sources of REEs seem to have emerged in the regions close to Japan. This indicates that the full range of possible sources of commercially viable REEs has not at all been fully explored.

Another reaction in Japan has been to look at the opportunities presented by recycling. Electronic waste is a rich source of REEs through recycling. Unused electronic goods in Japan alone are estimated to contain of the order of 300,000 Tonnes of REEs. Several industrial initiatives have been set up to tap into this opportunity. The extraction of metals from land-fill or urban waste is often referred to as “urban mining.” In the case of e-waste in Europe however it is problematic. E-waste is often classified as hazardous due to the presence of metals and other components that are ultimately seen as harmful to health or the environment, and therefore subject to strict controls in terms of handling and disposal. For this reason e-waste is often wrongly classified as “used goods” and exported without treatment.

In this way large quantities of strategically important minerals that could in principle be recovered and recycled are exported from Europe to landfill sites in far-away places such as Africa. One of the “incentives” for doing this seems to be the relatively high cost of recycling of e-waste. In actual fact many exciting and highly effective technologies now exist based on closed-loop chemical processes that enable the recovery of REEs in industry friendly forms, as useful oxides, alloys and mixtures. At the EIAS meeting a German company called Loser Chemie gave an excellent overview of what is nowadays possible. To be really effective these techniques need to be combined with sorting strategies that are “aware” of the REE content of e-waste. A more transparent and liquid market for REEs extracted in this way would help. According to the CTO of Loser Chemie, not even 1% of the potential for recycling REEs in Europe is currently being exploited. It seems that there are many entrepreneurial opportunities for those with the knowledge and vision to make the leap. It would be nice to have a better grasp of the size of the opportunity that represents for Europe. Maybe this is a good question for someone else to take up as a way of building upon the debate started by this initiative of the EIAS.

The final question is to ask “how did we end up in this position of crisis in 2010” to start with. According to an online MIT resource dealing with The Future of Strategic Natural Resources, the entire world is still in danger of a resource crisis. Since the 1960s, China developed a strong mineral policy that was in line with its own growth needs, its natural advantage in terms of high quality deposits and low labor costs, while the rest of the world sat by and allowed itself to become dependent on a single country to meet the majority of its needs. Our last though is what ne3ds to be done to avoid this kind of situation ever arising again.

14 October 2014, the EIAS (European Institute for Asian Studies) organized a briefing seminar on “Europe’s Rare Earth dependence on China – Future Perspectives”.

The Future Now Show

Shape the future now, where near-future impact counts and visions and strategies for preferred futures start.

Do we rise above global challenges? Or do we succumb to them? The Future Now Show explores how we can shape our future now – where near-future impact counts. We showcase strategies and solutions that create futures that work.

Every month we roam through current events, discoveries, and challenges – sparking discussion about the connection between today and the futures we’re making – and what we need, from strategy to vision – to make the best ones.

The Future Now Show October 2014

about 3-D printing and medicine, marketing made meaningful, balanced communities and …

Featuring

Lise Voldeng, CEO & Chief Creative Officer, Ultra-Agent Industries Inc.

Mylena de Pierremont, Board Member, World Future Society

Patrick Crehan, CEO and Founder, Crehan, Kusano & Associates

Markus Petz, Head of Special Projects & Development, Experience Alternative Tampere

3-D printing services are popping up everywhere, but, given their low scalability, where will their biggest impact be?

Patrick Crehan reckons that it will be in printing living things. Not whole beasts but organs, from skin (already available) to hearts. The panel discusses the ethical implications, pulling in the increasing ability to build life from DNA up. Sounds scary? It probably isn’t. Probably…

Talking about scary, what about massive corporations, whose wealth affords enormous power but whose primary driving force (shareholder value) is fundamentally amoral?

Mylena de Pierremont suggests that societal pressures (presumably fuelled by enhanced global communication and wider investor spread) are driving a new business model whereby things like transparency, sustainability and corporate responsibility equate to shareholder value. Maybe those ‘evil giants’ need not be defeated but can be converted.

Mark Petz introduces the ‘global village’, as typified by the balance4yourlife project, billed as a new form of ‘intentional community’ – a sustainable urban village firmly anchored in the modern, interconnected world. While global populations are increasingly migrating to cities and city living is proving the most sustainable, can this concept buck that trend? After all, modern communications are often making geographical proximity less important. The attraction of villages, green fields and trees aside, is the small inclusive community, for which humans have arguably evolved, the antithesis of the impersonal anonymity of city life. Is the global village then a potential model for the future, maybe alongside cities? And will we all be invited? – By Paul Holister, Editor

The Future Now Show September 2014

about Climate Change, Food, Social Revolution and …

Featuring

Lise Voldeng, CEO & Chief Creative Officer, Ultra-Agent Industries Inc.

Kirsten van Dam, Director & Founder, Out Of Office

Arjen Kamphuis, Futurist, Co-founder, CTO, Gendo

Hardy F. Schloer, Managing Director, Schloer Consulting Group

Arjen Kamphuis calls climate change humanity’s greatest threat. How will we deal with this and with resource depletion, as forecast famously by the Club of Rome in the ‘70s? Does the point of no return for a solution lie ahead or has it passed and, if so, with what consequences?

Kirsten van Dam poses a related critical question, how to feed an ever-increasing population in a time of diminishing resources? Will technology provide an answer, as it has done before, or does mass starvation threaten?

A re-run of the Rome model in 2005 forecast collapse for any reasonable input values. And how bad could runaway climate change become? Some suggest a reduction of the Earth’s carrying capacity to 2 million souls. One respectable commentator suggests that a transition to a lifeless new Venus is conceivable. A great threat indeed.

Joining the discussion are Hardy Schloer and moderator Lise Voldeng. Solutions might require complete abandonment of the cultural and economic models born with the Industrial Revolution. But how much pain is needed to bring about such a revolution?

Hardy Schloer sees a common thread in recent events such as the Arab Spring, ISIS, the troubles in Ukraine and more – the uprising of groups defined by cultural or ethnic heritage, united in their rage against the machine. Are we seeing the beginning of the end of the nation state (a relatively recent construct anyway)? Will a more natural new world order emerge, or an older one re-emerge? How ugly might the transition be?

These questions are discussed with Arjen Kamphuis, Kirsten van Dam and moderator Lise Voldeng and it is agreed that the recent revolution in global communications is central, now and for the future. Maybe borders are obstacles and traditional democracy is outdated. Maybe we need a sense of belonging and usefulness that is framed around humanity rather than a nation or economic interests. – By Paul Holister, Editor

Energy Innovation

Elon Musk is a South Africa-born, Canadian American business magnate, inventor, and investor. He is the CEO and CTO of SpaceX, CEO and chief product architect of Tesla Motors, and chairman of SolarCity. He is the founder SpaceX and considered by many to be the cofounder of PayPal,] Tesla Motors, and Zip2. He has also envisioned a conceptual high-speed transportation system known as the Hyperloop.

Steven Chu is an American physicist who served as the 12th United States Secretary of Energy from 2009 to 2013. Chu is known for his research at Bell Labs in cooling and trapping of atoms with laser light, which won him the Nobel Prize in Physics in 1997, along with his scientific colleagues Claude Cohen-Tannoudji and William Daniel Phillips. At the time of his appointment as Energy Secretary, he was a professor of physics and molecular and cellular biology at the University of California, Berkeley, and the director of the Lawrence Berkeley National Laboratory, where his research was concerned primarily with the study of biological systems at the single molecule level. Previously, he had been a professor of physics at Stanford University. He is a vocal advocate for more research into renewable energy and nuclear power, arguing that a shift away from fossil fuels is essential to combating climate change.

Elon Musk and Steven Chu at the energy innovation Summit 2014

Club of Amsterdam blog

Club of Amsterdam blog

http://clubofamsterdam.blogspot.com

Socratic Design

by Humberto Schwab, Philosopher, Owner, Humberto Schwab Filosofia SL, Director, Club of Amsterdam

The Ukrainian Dilemma and the Bigger Picture

by Hardy F. Schloer, Owner, Schloer Consulting Group – SCG, Advisory Board of the Club of Amsterdam

The impact of culture on education

by Huib Wursten, Senior Partner, itim International and

Carel Jacobs is senior consultant/trainer for itim in The Netherlands, he is also Certification Agent for the Educational Sector of the Hofstede Centre.

What more demand for meat means for the future

by Christophe Pelletier, The Happy Future Group Consulting Ltd.

Inner peace and generosity

by Elisabet Sahtouris, Holder of the Elisabet Sahtouris Chair in Living Economies, World Business Academy

News about the Future

Implants That Trigger Self-Healing

DARPA’s ElectRx program plans to develop technologies to restore and maintain healthy physiological status through monitoring and targeted regulation of signaling in peripheral nerves that control organ functions. Novel therapies based on targeted stimulation of the peripheral nervous system could promote self-healing, reduce dependence on traditional drugs and provide new treatment options for illnesses.

ElectRx is also expected to improve peripheral nerve stimulation treatments for brain and mental health disorders, such as epilepsy, traumatic brain injury (TBI), Post-Traumatic Stress Disorder (PTSD) and depression.

Achieving DARPA’s goals for the program would require new technologies for in vivo sensing and neural stimulation, including advanced biosensors and novel optical, acoustic and electromagnetic devices to achieve precise targeting of individual or small bundles of nerve fibers that control relevant organ functions.

“The technology DARPA plans to develop through the ElectRx program could fundamentally change the manner in which doctors diagnose, monitor and treat injury and illness,” said Doug Weber, DARPA program manager. “Instead of relying only on medication—we envision a closed-loop system that would work in concept like a tiny, intelligent pacemaker. It would continually assess conditions and provide stimulus patterns tailored to help maintain healthy organ function, helping patients get healthy and stay healthy using their body’s own systems.”

Adenosine can melt “love handles”

Researchers at the University of Bonn discover a new signaling pathway to combat excess body weight.

The number of overweight persons is greatly increasing worldwide – and as a result is the risk of suffering a heart attack, stroke, diabetes or Alzheimer’s disease. For this reason, many people dream of an efficient method for losing weight. An international team of researchers led by Professor Alexander Pfeifer from the University Hospital Bonn, have now come one step closer to this goal. The scientists discovered a new way to stimulate brown fat and thus burn energy from food: The body’s own adenosine activates brown fat and “browns” white fat.

“Not all fat is equal,” says Professor Alexander Pfeifer from the Institute of Pharmacology and Toxicology of the University Hospital Bonn. Humans have two different types of fat: undesirable white fat cells which form bothersome “love handles”, for example, as well as brown fat cells, which act like a desirable heater to convert excess energy into heat. “If we are able to activate brown fat cells or to convert white fat cells into brown ones, it might be possible to simply melt excess fat away” reports the pharmacologist.

“If adenosine binds to this receptor in brown fat cells, fat burning is significantly stimulated,” reports Dr. Thorsten Gnad from Prof. Pfeifer’s team. It was previously thought not possible for adenosine to activate brown fat. Several studies with rats and hamsters demonstrated that adenosine blocks brown fat.

Recommended Book

The Future of Continental Philosophy of Religion

by Clayton Crockett (Editor), B. Keith Putt (Editor), Jeffrey W. Robbins (Editor)

What is the future of Continental philosophy of religion? These forward-looking essays address the new thinkers and movements that have gained prominence since the generation of Derrida, Deleuze, Foucault, and Levinas and how they will reshape Continental philosophy of religion in the years to come. They look at the ways concepts such as liberation, sovereignty, and post-colonialism have engaged this new generation with political theology and the new pathways of thought that have opened in the wake of speculative realism and recent findings in neuroscience and evolutionary psychology. Readers will discover new directions in this challenging and important area of philosophical inquiry.

The AsianSquare Dance – 1st part

By Michael Akerib, Vice-Rector, SWISS UMEF UNIVERSITY

Goldman Sachs first coined the expression BRICs – Brazil, Russia, India and China – to identify the economic giants of the future that will reshape the world economic order. While Russia’s economy is linked to the prices of commodities, energy in particular, Brazil has not lived up to expectations. Of the four countries, China and India have shown the most impressive growth in recent years with, respectively, 10% and 8%. Excluding Brazil, the population of the BRIC represents 40% of the world’s inhabitants.

With Asia, reckoned to be today the most dynamic continent, accounting for 65% of the world’s population, and China and India together accounting for 40%, these two countries can potentially alter the fragile equilibrium of the world’s economy. It is forecast that by 2030 the East Asian economies will be the world’s largest economic bloc.

Due to diverging political ideologies and concerns, however, this bloc does not, in fact, exist other than in prose. Even worse, all the countries in the area have made significant investments in military equipment over the recent past thus sharply increasing the risk of conflict particularly as fears grow over China’s intentions.

The US’ dream, during the cold war, of creating an Asian equivalent to NATO was short lived. Today, Asia has five nuclear powers: Pakistan, India, China, North Korea and Russia. On the other hand, the US is constrained by budgetary problems.

Our argument in this series of articles is that the development of Asia, and its impact on the rest of the world, depends to a large extent on the relations between five countries: China, India, Japan, South Korea and the US. Depending on the structure of the type of relations that will develop, and choices made by Russia and the US, for instance on their energy policy, we may see a new world order developing, very different from that of the last four hundred years. Further, if the Chinese economy faces difficulties in the future, the US will be instrumental in determining Asia’s future. Conversely, if the US economy falters, China, if it so wishes, could assume the world’s economic leadership.

Since the end of the Second World War, the US’ role in the area has been a major influencing factor politically, militarily and economically and while it has declined recently, it remains, nevertheless, important. Asia is challenging the EU as the world’s most important trade bloc.

The US imports from Asia for over $2 trillion per year, thus making the US responsible for the creation of hundreds of thousands of jobs. A weakening of the US dollar could significantly diminish the US’ role in the region.

At issue here is what A F K Organski has termed ‘Power transition theory’ – i.e. the change of the guard of the dominant power where the dominant power occupies this position because of its control of resources, be they demographic, economic, geographic, natural or military.

According to the theory, the dominant power, or powers, must ensure the stability of the system failing what the system might be challenged by an emerging hegemon. These situations are conducive to confrontation, very often military.

The emerging hegemon is, no doubt, China, and the events in Eurasia, over the coming quarter century will witness an indirect confrontation between China and the US, a confrontation whose secondary actors are India and Russia.

Is China striving to attain the status of great power and challenge the US, at least regionally, and what role do the other regional powers, as well as Russia and the US play? Or is it just trying to reduce its feeling of being surrounded by enemies?

Asia has become a powerhouse with several countries showing economic strength and appearing to be rivals. A dangerous rivalry inasmuch as five countries in the area have a nuclear arsenal (China, India, North Korea, Pakistan and Russia), with two more (Japan and South Korea) able to produce a nuclear bomb in a relatively short time.

Monetary reserves in Asia are sufficient to allow the area to develop without much further foreign investments. Further, an increase in economic stability is heralded by the recent agreement between several Asian countries – the members of ASEAN, China, Japan and South Korea – to pool their financial resources in case of a speculative attack.

While the major trade partner of most of the countries in the area is Australia, the European Union and the United States, regional trade has increased considerably. Services such as tourism also cater increasingly to Asians.

There remains the question of whether the continent is able to develop its own technological base to compete with Europe and the US. There are diverging points of view on the issue.

The perception by the Asian countries of the effect of China’s domination of the continent evolved into an understanding that they only have two options – siding with China or with Japan and its US ally.

The financial difficulties originating in the US and which have spilled all over the world have affected Asia in its role of major exporter. As a reaction, China, Japan and South Korea are considering the creation of a community modelled on the European Union that would help them expand trade within their area and increase trade with the ASEAN countries, Russia, the Middle East and Europe. They are encouraged in this action as inter-Asian trade has been growing at twice the rate of global trade. Inter-Asian trade is more important as a percentage of total trade than inter-NAFTA trade.

The US should fear the creation of a trading block including China, Japan and South Korea as it would represent 43% of US’ foreign trade and holdings of over one trillion dollars in US Treasury paper.

Common problems

The countries in the area, with the notable exception of Russia, share two major problems: access to raw materials in general, and energy in particular, and an economy essentially geared to exports, and thus very dependent on the purchasing power of EU and US consumers. This last aspect is changing rapidly though with domestic markets starting to take shape and offering local producers a partial insulation from the American-led boom and bust cycles.

It is generally felt in the US that China has not been doing enough to stimulate internal demand – the number of consumers is no bigger than Italy while the population is 20 times that of the European country – and that the situation has been worsened by the decision of the Chinese government to peg the Yuan to the US dollar, thus effectively undertaking a devaluation.

Should China’s export drive remain as a major contributor the country’s economy, the accumulation of reserves by 2020 will be bigger than that of Germany, Japan and the Middle East countries put together. America’s response could be to return to a more isolationist policy by slapping import duties on Chinese products or getting China to open its doors to greater exports of US products.

Both China and India have to contend with an extremely large population. In fact, they are the only two countries with a population of over 1 billion persons. Economic development has brought, to both countries, an uneven distribution of wealth to the extent that social disruptions can be feared in the future.

China has become the world’s second largest oil consumer and it is likely that it will surpass the US to lead the world in energy use. Imports which represent 50% of consumption are likely to rise to reach 80% in another 10 – 15 years particularly considering the oil intensity of economic growth is particularly high, as in most developing countries. Thus, for each 1% growth in GDP, the country needs 1.2% additional oil.

In fact, China is the world’s fast-growing energy user, Russia is the most inefficient user of energy and he US is the country with the largest carbon footprint.

China is also the world’s largest consumer of several raw materials.

The country’s search for natural resources has been done in a predatory way, and there is fear that, backed by its staggering reserves, it could encourage suppliers to increase prices at levels beyond those acceptable to a large number of other users.

India’s energy requirements are expected to grow by 30% in the next 3 to 5 years and its imported crude oil dependency is expected to reach 95% by 2025.

India depends for 50% of its energy needs on coal and increasing its use would create major environmental problems.

Its gas suppliers are considered to be relatively unreliable and include Bangladesh, Iran, Myanmar and Turkmenistan.

This situation has encouraged India to pursue the road to nuclear power.

Such growth in raw material requirements is not sustainable and is strategically dangerous.

Both China and India have very large armies (in fact the largest in the world) and nuclear weapons.

Japan is also a major energy importer, relying entirely on imports for oil. Japan has an important stockpile of energy products, and it has encouraged other Asian countries, including China, to jointly plan the stocks and their administration.

Indeed, Asia’s energy needs are expected to double in the coming 20 years. In spite of this, OPEC countries do not seem to be prepared to invest in increasing production, in large part because of the massive funds required. They have been estimated by McKinsey to be of the order of $ 45 billion a year over the next three decades.

The countries in the area perceive themselves as rivals in securing energy sources and China, particularly, has shown an eagerness to develop partnerships, whether through limited investments, or through political support, in the United Nations, of countries like Iran.

Hydrocarbon reserves in the China Sea are claimed by several countries, and are a growing point of contention. Neighboring countries are fearful of China’s rising military power and have led them to develop closer relations with the US.

In an effort to temper their competition, India and China have made some joint bids to buy and share oil fields.

Japan too is dependent on energy imports and has recently been unlucky with their supply sources. Thus, they have had to curtail their investments in Iran, Kuwait, Russia and Saudi Arabia.

To counterbalance these losses, Japan has offered Saudi Arabia the possibility of building oil-storage facilities in Okinawa, provided Japan can have access to them in case of emergency.

A closer rapprochement between the two countries depends, however, on the US’ willingness for this to take place as the Saudi monarchy depends on the US military shield against the rising threat of Iran and of the djihadists, and there is no way Japan can replace the US in that role. This, in spite of the fact that Asia is today, by far, the largest buyer of both Saudi and more generally, Middle Eastern oil – up to 60% and 70% of their exports, respectively.

Reliance on Russia for energy is therefore extremely important. While a pipeline is being built from Siberia to the Pacific that could partly alleviate these escalating needs, a number of other pipeline projects have been proposed. All these projects require large investments ($ 1-2 million per kilometer of pipeline or around $ 12 billion for the pipeline that will link Russia and China), long delays in building and face substantial political and ecological problems. Further, the gas transmission systems in China and Japan are under-developed and therefore not suitable for the transport of large quantities of imported gas.

Russian industry has access to gas supplies at prices substantially below those practised on world markets and has therefore become a voracious user. The Russian government will be increasing prices for domestic consumption, including for private heating, and / or turning to alternative energy sources such as coal, hydro-electric or nuclear power.

Other possibilities have also been considered, but they all depend on Russia’s cooperation.

Thus, for instance, integrating the energy grids of Russia with those of China, Japan and the two Koreas has been proposed to enable the exchange of seasonal surplus.

This entails not only Russia’s cooperation, but also North Korea’s. It also requires large investments, although possibly not of the scale of building a pipeline network.

Another common point between the China, India, Japan and South Korea is that they constitute, jointly, the world’s largest weapons market and their suppliers are the European Union, Russia and the United States.

China and Japan also share the will to stop North Korea’s nuclear program.

The two countries are also large emitters of greenhouse gases.

Both China and Russia fear, perhaps rightly so, that the US is conducting an encirclement strategy due to their military presence in Central Asia as well as, in Japan, South Korea and Taiwan as far as China is concerned, and Russia is concerned with a possible NATO expansion in Europe.

ISIS and Western intelligence role in the Middle East

ISIS and Western intelligence role in the Middle East by Annie Machon.

” … We can’t defeat terrorism by war! …”

Machon is a former intelligence officer for MI5, the UK Security Service, who resigned in 1996 to blow the whistle on the spies’ incompetence and crimes. Drawing on her varied experiences, she is now a media pundit, author, journalist, political campaigner, and PR consultant.

Futurist Portrait: Geci Karuri-Sebina

Geci Karuri-Sebina

Chair & Director: South African Node at The Millennium Project

Executive Manager: Programmes at SA Cities Network

Research Associate: Institute for Economic Research on Innovation (IERI)

Geci’s interests are broadly in foresight and R&D spanning a range of public policy, development, and innovation issues. She is actively involved in the futures study field which she champions through her role as a founding member and director of the SA Node of the Millennium Project.

She holds an MA in Urban Planning, and a Masters in Architecture and Urban Design from the University of California Los Angeles (UCLA) and a PhD in development planning and innovation from the University of Witwatersrand.

Geci Karuri-Sebina: … “Johannesburg hopes to be a vibrant, equitable, diverse, sustainable, resilient and adaptive city by 2040, a vision that will require rigorous engagement and monitoring over time, in unfolding contexts.

…

As a foresight enthusiast and practitioner, Johannesburg’s growth and development vision appeals greatly. Not because it will accurately predict or enable a specific outcome – “a world class African city”, “a city of our dreams”, “a city growing with you”, or “a city that works for me,” as various cities across South Africa have outlined in their catchy slogans – but because espousing a view to the future is a basic prerequisite of visionary action. It is a bold move, creating the potential to focus and capture the imaginations of the co-creators and constituents of that future. A basic question remains: What exactly is the future that we see for the entirety of our city? Before we begin talking of GDS 2050, perhaps we should attempt a shared peek from the mountaintop, to see if there is a believable and grounded promised land ahead, with clear signs behind, and many signposts in between.” Source: CityScapes

Geci Karuri-Sebina, South Africa Node of the Millennium Project, Baku Futures Forum

Agenda

| Season Events 2014 / 2015 UK the future of Collective Intelligence January 28, 2015 Location: The Cube, Studio 5, 155 Commercial Street, London E1 6BJ This is a collaboration between The Cube and the Club of Amsterdam. UK the future of Metro Vitality Aprll 24, 2015 Location: London This is a collaboration between APF and the Club of Amsterdam |

Customer Reviews

Thanks for submitting your comment!